If you started a monthly SIP of 10,000 back in 2016, chances are you are still investing 10,000 today. Your salary has likely doubled in that time. Your rent has gone up. Your groceries cost more. But your mutual fund investment? It has stayed exactly the same for a decade.

This is the single most common investing mistake Indian SIP investors make, and it quietly costs them crores over a 15-20 year horizon.

Here is the number that puts it in perspective. A flat 10,000/month SIP at 12% annual return for 20 years grows to approximately 1 crore. The same SIP, with a simple 10% annual step-up, grows to approximately 1.99 crore. Same starting point. Same fund. Same return assumption. Nearly double the corpus, purely from increasing the monthly amount by 10% each year.

And yet, most Indian investors never set up this one adjustment. According to AMFI, SIP monthly inflows hit an all-time high of 32,087 crore in March 2026, with 9.72 crore accounts actively contributing. By May 2026, SIP AUM stood at 17,12,126 crore, accounting for roughly 21% of the entire mutual fund industry’s assets. India’s SIP culture is stronger than ever. But the average SIP ticket size remains approximately 3,167 per month (AMFI data), and the majority of these SIPs run at a flat amount year after year.

This guide explains exactly how step-up SIP works, walks through the real math behind different increment percentages, shows when stepping up makes sense and when it does not, and covers practical setup and common mistakes. If you are still deciding between SIP and lump sum investing as your base strategy, we covered that comparison in depth here. Step-up SIP is the next step after that decision is made.

What is Step-Up SIP: How It Works in India ?

A step-up SIP (also called a top-up SIP) is a systematic investment plan where your monthly contribution increases automatically by a fixed percentage or a fixed rupee amount at regular intervals, typically once a year. Instead of investing the same 10,000 every month for the entire tenure, your SIP amount grows annually, putting progressively more capital to work in the market.

There are two types of step-up:

- Percentage-based step-up: Your monthly SIP increases by a set percentage each year. A 10,000 SIP with a 10% annual step-up becomes 11,000 in year 2, 12,100 in year 3, 13,310 in year 4, and so on. The growth is exponential.

- Fixed-amount step-up: Your monthly SIP increases by a fixed rupee amount each year. A 10,000 SIP with a 1,000 annual step-up becomes 11,000 in year 2, 12,000 in year 3, 13,000 in year 4. The growth is linear.

Why does this exist? Because it mirrors how most Indian salaried professionals actually earn money. Corporate salary increments in India typically range from 8-15% annually. A step-up SIP captures a portion of each raise and channels it into investing before lifestyle spending absorbs it entirely. You set it once during SIP creation, and the platform handles the annual increase automatically. No fresh KYC, no new folio, no yearly paperwork.

The minimum SIP for step-up is typically 500-1,000/month on most platforms, with step-up increments as low as 500/year (fixed) or 5% (percentage). And the flexibility is important: most AMCs and investing platforms allow you to modify, pause, or completely stop the step-up at any time without affecting your base SIP. Your original monthly amount continues running even if you freeze the step-up during a financially tight year.

Step-Up SIP vs Regular SIP: The Numbers That Change Everything

Theory only matters if the math backs it up. So let us put the two approaches side by side across three different investment horizons with a starting SIP of 10,000/month and an assumed 12% annual return.

10-Year Comparison

- Flat SIP: Total invested: 12 lakh. Estimated corpus: approximately 23.23 lakh.

- 5% annual step-up: Total invested: approximately 15.09 lakh. Corpus: approximately 28.9 lakh.

- 10% annual step-up: Total invested: approximately 19.12 lakh. Corpus: approximately 36.15 lakh.

- 15% annual step-up: Total invested: approximately 24.35 lakh. Corpus: approximately 45.58 lakh.

Even over just 10 years, a 10% step-up produces a corpus that is 55% larger than a flat SIP. The invested amount is higher too, naturally, but the compounding on those increased contributions does the heavy lifting.

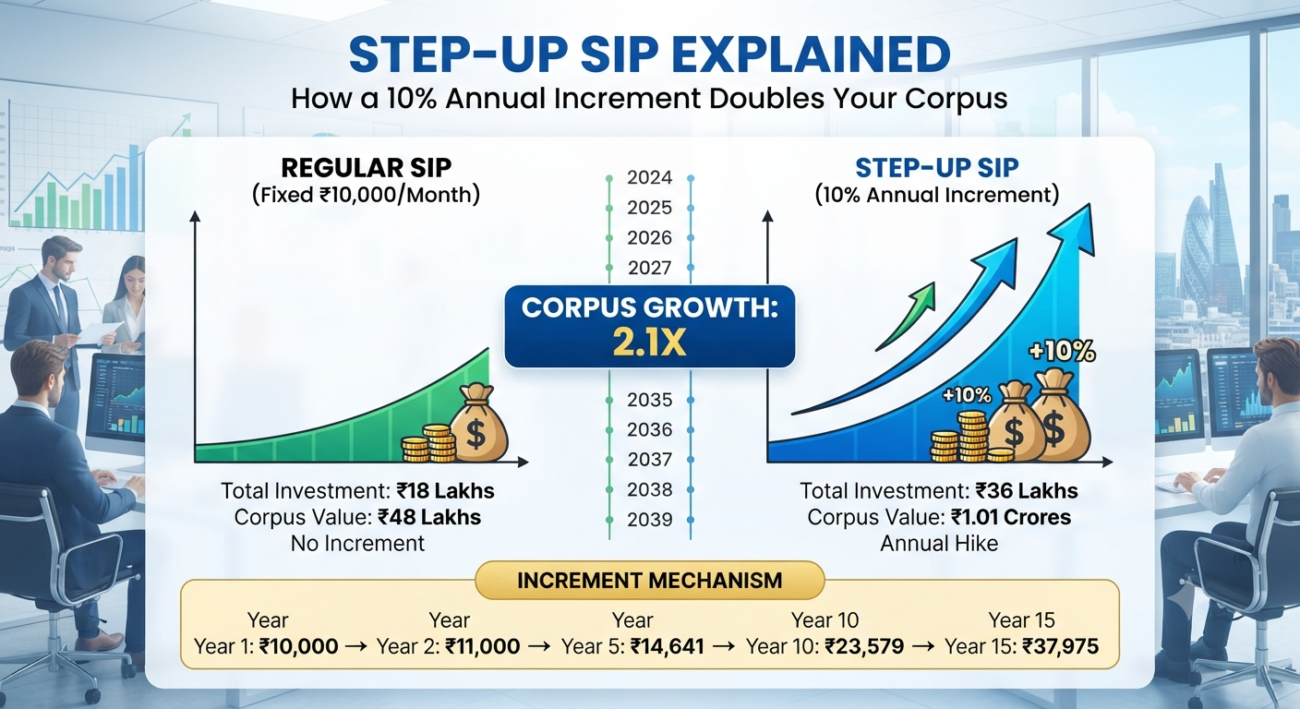

15-Year Comparison

- Flat SIP: Total invested: 18 lakh. Corpus: approximately 50.46 lakh.

- 5% step-up: Total invested: approximately 26.63 lakh. Corpus: approximately 73.28 lakh.

- 10% step-up: Total invested: approximately 38.17 lakh. Corpus: approximately 1.06 crore.

- 15% step-up: Total invested: approximately 56.27 lakh. Corpus: approximately 1.59 crore.

This is where the gap starts becoming dramatic. A 10% step-up crosses the 1 crore mark in 15 years. The flat SIP reaches only 50 lakh. The step-up investor has more than double the corpus with roughly 2.1x the total investment.

Value Research published a detailed comparison in February 2026 that illustrates this perfectly. Two investors, Priya and Pallavi, started SIPs on the same date, in the same fund, with the same monthly amount. After 15 years, Pallavi had approximately 72 lakh while Priya had only 40 lakh. The difference? Pallavi stepped up her SIP by 10% every year with each salary increment. The return assumption was identical. What changed was the invested amount and how long each increased installment had to compound.

20-Year Comparison

- Flat SIP: Total invested: 24 lakh. Corpus: approximately 99.9 lakh (roughly 1 crore).

- 5% step-up: Total invested: approximately 39.68 lakh. Corpus: approximately 1.44 crore.

- 10% step-up: Total invested: approximately 68.73 lakh. Corpus: approximately 1.99 crore.

- 15% step-up: Total invested: approximately 1.22 crore. Corpus: approximately 3.44 crore.

The 20-year numbers are the most cited in the industry, and for good reason. A 10% step-up nearly doubles the corpus compared to a flat SIP. At 15%, the corpus is 3.4x the flat SIP corpus. As Sahi.com summarized in a recent analysis: a flat 10,000 SIP at 12% for 20 years gives 99.9 lakhs, while the same SIP with a 10% annual step-up gives approximately 1.99 crore, almost double, purely from disciplined annual increments.

The critical takeaway across all three horizons: the return assumption never changed. The fund performance was identical. The only variable was the investor’s decision to increase their monthly contribution by a modest percentage each year. That single decision, compounded over time, is worth crores.

How a 10% Annual Step-Up Actually Works Year by Year ?

Numbers in a comparison table can feel abstract. So here is what a 10,000/month SIP with a 10% annual step-up looks like in practice for the first five years:

- Year 1: 10,000/month. Total invested that year: 1,20,000.

- Year 2: 11,000/month. Total invested: 1,32,000.

- Year 3: 12,100/month. Total invested: 1,45,200.

- Year 4: 13,310/month. Total invested: 1,59,720.

- Year 5: 14,641/month. Total invested: 1,75,692.

By year 10, the monthly SIP amount reaches 23,579. By year 15, it is 37,975. By year 20, you are investing 61,159 per month.

That year-20 number might look intimidating right now, but consider the context. If your salary grows at even 8-10% per year (the Indian corporate average), your income in year 20 will be 4-6 times what it is today. An SIP of 61,159 on a monthly income of 3-4 lakh is roughly the same proportion as 10,000 on today’s 60,000-80,000 salary. The ratio stays manageable because both your income and your SIP grow in parallel.

There is also a compounding mechanic that makes step-up SIP especially powerful. The year-1 installments compound for the full 20 years. The year-2 installments (now at a higher amount) compound for 19 years. Each subsequent year’s higher contribution stacks on top of the earlier compounding. This layered compounding effect is where the corpus difference comes from. It is not just that you invested more money. It is that the additional money had time to grow.

A practical tip: if you receive your salary increment in April, set your step-up SIP to increase in April or May as well. This way, the higher SIP amount coincides exactly with the higher paycheck, and you never feel the increase in your monthly budget.

Percentage Step-Up vs Fixed-Amount Step-Up: Which Should You Choose

This is a decision most investors do not think about carefully, but it matters more than it appears, especially over long tenures.

Percentage-based step-up (e.g., +10% per year)

The increase scales naturally with the growing SIP amount. In year 2, a 10% increase on 10,000 adds 1,000. But in year 15, a 10% increase on 37,975 adds 3,797. The absolute rupee increase gets larger every year, which means more capital is deployed into the market as time goes on. This mirrors how percentage-based salary increments work, making it the more natural fit for salaried professionals. Percentage step-up is best suited for long tenures of 15 years or more, where the acceleration in later years creates the biggest compounding impact.

The risk: if your income growth stalls or you face a financially difficult period in year 8 or 10, the absolute amount being demanded by your SIP could exceed what is comfortable. This is why setting a cap matters (covered in the next section).

Fixed-amount step-up (e.g., +1,000 per year)

The increase is the same rupee amount every year. 10,000 becomes 11,000, then 12,000, then 13,000. Growth is linear and completely predictable. You know exactly what your SIP will be in year 5 or year 10 without needing a calculator. This is simpler to budget around and works well for investors with irregular income or those who prefer predictability over optimization.

The limitation: a fixed 1,000 increase on a 10,000 SIP is a 10% bump. But the same 1,000 increase on a 25,000 SIP (which you will have by year 15) is only a 4% bump. The real step-up rate declines over time, which means the compounding advantage weakens in the later, most impactful years.

Which to choose? Finnovate Research offered a practical framework: if your salary typically grows 6-10% annually, pick a 5-10% percentage step-up. If increments are uneven or you prioritize predictability, use a fixed rupee step-up and review yearly. For most salaried investors in India with stable corporate jobs, a percentage-based step-up of 10% is the default recommendation. Sync the step-up month with your annual appraisal month so the increase maps directly to your salary revision.

Why Step-Up SIP Beats Inflation (and Regular SIP Does Not)

India’s consumer price inflation has averaged 5-7% over the past decade. What this means in practical terms: 10,000 today will have the purchasing power of roughly 5,500 in 10 years at 6% inflation. If you are running a flat SIP of 10,000/month and never increasing it, your real investment is actually shrinking every year in inflation-adjusted terms. You are putting in the same number of rupees, but each rupee buys less.

A 10% annual step-up comfortably outpaces this erosion. By year 10, your monthly SIP is 23,579, which, adjusted for 6% inflation, still represents a meaningfully higher real contribution than the original 10,000. Your invested amount is not just keeping pace with rising costs. It is growing ahead of them.

This matters most for specific goal categories where inflation runs even higher than the general average:

- Education inflation in India: 8-10% per year. College fees that cost 10 lakh today will cost 21-26 lakh in 10 years. For a child education SIP, a 10% step-up is the minimum recommended increment.

- Healthcare inflation: 10-15% annually. A retirement corpus planned on flat SIP contributions will fall short of actual medical expenses in later years.

- Real estate: Property prices in metro cities have historically appreciated 7-9% per year. A house down payment goal needs the SIP to grow alongside property prices.

The bottom line: a flat SIP is a nominal commitment. A step-up SIP is a real commitment that maintains its value over the full investment horizon.

Setting a Cap: The Safety Valve Most Investors Ignore

Here is a number that surprises most people: a 10,000/month SIP with a 10% annual step-up reaches 61,159 per month by year 20. That is over 7.3 lakh per year in SIP contributions alone. If your income growth does not keep pace, or if life throws unexpected expenses at you, this amount can become a source of financial stress rather than financial growth.

This is why setting a monthly cap is critical when you create a step-up SIP. Most platforms (Groww, Zerodha Coin, Kuvera, Paytm Money) allow you to specify a maximum monthly amount. Once your SIP reaches that cap, it stays flat for the remaining tenure instead of continuing to increase.

For example: set your starting SIP at 10,000 with a 10% annual step-up and a cap of 30,000. The SIP increases every year until it hits 30,000 (around year 12), then stays at 30,000 for the remaining 8 years. You still get the compounding benefit of the step-up years, but you are protected from overcommitting in later years.

Tips for setting the right cap:

- A safe ceiling is 30-40% of your current monthly take-home income. If you earn 80,000/month, cap the step-up SIP at 24,000-32,000.

- Review the cap every 2-3 years and adjust upward if your income has grown faster than expected.

- If you are running multiple SIPs across different funds, calculate the combined step-up trajectory, not just individual SIPs. Three SIPs of 10,000 each, all with 10% step-up, collectively reach 1,83,477/month by year 20.

- The AMFI SIP stoppage ratio crossed 100% in both March and April 2026, meaning more SIP accounts ended than started. Overcommitting to aggressive step-ups without a cap is one contributing factor. A stopped SIP generates zero wealth. A capped SIP that continues for the full tenure generates far more than an uncapped one that gets abandoned in year 6.

The guiding principle: choose a step-up percentage and a cap that you can sustain through a bad year, not just a good one. The best step-up SIP is the one that keeps running.

How to Set Up a Step-Up SIP on Major Indian Platforms

Setting up a step-up SIP takes less than five minutes on most investing platforms. The process is nearly identical to starting a regular SIP, with one additional step where you specify the annual increment. Here is how it works on the platforms most Indian investors use:

Groww: Select your mutual fund scheme, choose SIP as the investment mode, enter your monthly amount, then enable the “Annual Step-Up” toggle that appears below the amount field. Enter your preferred step-up percentage (options typically range from 5% to 25%). You can also set a maximum cap. Confirm your e-mandate and the step-up is active.

Zerodha Coin: During SIP setup, select the “Step-Up” option after entering the base monthly amount. Choose between percentage-based or fixed-amount increment, enter the value, set an optional cap, and confirm. The mandate adjusts automatically each year.

Kuvera: Set up a regular SIP first, then use the “Top-Up” option within SIP settings. You can choose a percentage or fixed-amount increase and specify the frequency (annual is standard). Kuvera also shows a projection of what your SIP amount will look like in future years before you confirm.

Paytm Money: The SIP setup flow includes the step-up option directly. Enter your base amount, select the step-up percentage, review the year-wise projection, and confirm.

AMC Direct (Nippon India, HDFC, SBI, ICICI Prudential): Most AMC websites and apps now offer “SIP with Annual Increase” as a standard option during mandate creation. The interface varies by AMC, but the inputs are the same: base amount, increment type, increment value, and optional cap.

The key point: the step-up mandate is configured once at the time of SIP creation. After that, there is no yearly paperwork, no fresh KYC, no new folio number. The platform handles the annual increase automatically on the anniversary of your SIP start date.

If your current platform does not support automatic step-up (some older AMC portals may not), you can achieve the same result manually by stopping the existing SIP at the end of each year and starting a new one with the higher amount. This works but requires annual effort and discipline, which is exactly the behavioral gap that automatic step-up eliminates.

When NOT to Use Step-Up SIP: The Risks Nobody Talks About

Step-up SIP is not a universally correct choice. There are specific scenarios where it can backfire, and understanding these is just as important as understanding the math.

Stepping up faster than your income grows. This is the most common mistake. An investor chooses a 15% annual step-up because the corpus projections look impressive, but their actual salary increment averages only 8%. By year 4 or 5, the SIP amount exceeds what their budget can comfortably support. The result? They stop the SIP entirely. A stopped SIP generates zero wealth. A flat SIP that continues uninterrupted for 15 years generates far more than an aggressive step-up SIP that gets abandoned in year 5.

The AMFI data from 2026 confirms this risk at scale. The SIP stoppage ratio crossed 100% in both March and April 2026, meaning more SIP accounts ended or completed their tenure than new ones started. While multiple factors drive stoppages (including tenure completions and the Nifty 9.37% fall in March 2026), overcommitting to SIP amounts that become unaffordable is a documented contributor. SIP monthly inflows remained strong at 30,953 crore in May 2026, but the account-level contraction signals that sustainability matters more than ambition.

Not having an emergency fund in place. If you do not have 3-6 months of essential expenses saved in a liquid fund, committing to annual SIP increases adds financial fragility. A job loss, medical emergency, or major unexpected expense during a year when your SIP just stepped up can force you to break the SIP at the worst possible time.

Goals less than 5 years away. For short-term targets like a vacation fund, wedding expenses, or a car purchase within 3-5 years, step-up SIP adds minimal compounding benefit. The increments do not have enough time to compound meaningfully. A flat SIP into a liquid or ultra-short-duration fund is sufficient for short horizons.

Near retirement (5 years or less to withdrawal). Increasing equity exposure as you approach your withdrawal date adds sequence-of-return risk. If the market drops 15% in the final year and your stepped-up SIP has been adding more units at higher NAVs, the timing works against you. For near-retirement investors, additional savings should go into debt mutual funds or hybrid conservative funds, not equity step-ups.

Investing in the wrong fund category. Stepping up contributions into a sectoral or thematic fund (banking, IT, pharma, defence) concentrates risk over time. Each year’s higher SIP amount goes into the same narrow sector. Step-up SIP works best with diversified equity funds: flexi-cap, large-and-mid-cap, multi-cap, or broad market index funds like Nifty 50 or Nifty 500.

Tax Implications of a Larger Step-Up SIP Corpus

A bigger corpus is a good problem to have, but it comes with a tax planning requirement that most step-up SIP investors overlook until redemption time.

Current equity mutual fund tax rates for FY 2025-26 (unchanged by Budget 2026):

- STCG (Short-Term Capital Gains): 20% on gains from units held less than 12 months, under Section 111A.

- LTCG (Long-Term Capital Gains): 12.5% on gains exceeding 1.25 lakh per financial year from units held over 12 months, under Section 112A. The first 1.25 lakh of LTCG each year is tax-free.

Here is where the step-up SIP creates a specific tax consideration. A flat 10,000 SIP over 20 years invests 24 lakh and creates a corpus of approximately 1 crore. The capital gain is roughly 76 lakh. A 10% step-up SIP invests 68.73 lakh and creates approximately 1.99 crore. The capital gain is roughly 1.30 crore. The absolute LTCG liability on the step-up corpus is significantly higher, even though the tax rate is the same 12.5%.

Tax harvesting strategy: The most effective approach is to redeem gains up to 1.25 lakh each financial year to fully use the annual LTCG exemption, then reinvest immediately. There is no mandatory cooling-off period under Indian tax law before re-entering the same fund. Over a 5-7 year pre-retirement window, this strategy can save lakhs in taxes by systematically extracting gains within the exemption limit.

Also important: SIP redemptions follow FIFO (First In, First Out) rules. Each monthly installment has its own purchase date and holding period. When you redeem, the oldest units are sold first. For a step-up SIP that has been running for 10+ years, the earliest installments (which have compounded the most and have the highest gains) will be the first to be sold. Plan partial redemptions carefully to avoid triggering a large LTCG bill in a single financial year.

ELSS note: If you are running a step-up SIP in an ELSS (Equity Linked Savings Scheme) for Section 80C benefits under the old tax regime, remember that the 80C deduction is capped at 1.5 lakh per year. A step-up SIP exceeding 12,500/month goes beyond the 80C limit. The excess amount still gets invested and locked for 3 years, but without any additional tax benefit. Balance your ELSS allocation accordingly if you are using the old tax regime.

Step-Up SIP for Specific Financial Goals

The power of step-up SIP varies dramatically based on your goal horizon. Here is how to calibrate the step-up percentage for the most common Indian investor goals:

Child’s Higher Education (15-18 year horizon)

Education costs in India have been inflating at 8-10% annually. An engineering degree that costs 8 lakh today could cost 25-35 lakh by the time your child reaches college. A flat SIP grossly underestimates this inflation. Recommended approach: start with 5,000/month, set a 10% annual step-up, invest in a flexi-cap or large-and-mid-cap fund. At 12% assumed return over 15 years, this creates approximately 53 lakh, compared to just 25 lakh with a flat SIP. The step-up more than doubles the education fund.

Retirement Corpus (20-25 year horizon)

This is where step-up SIP has its most dramatic impact. A 10,000/month SIP with a 10% annual step-up for 25 years at 12% return creates approximately 4.7 crore. The same flat SIP creates approximately 1.88 crore. The step-up investor retires with nearly 2.5 times the corpus, which translates directly into a higher monthly withdrawal in retirement. Given healthcare inflation of 10-15% in India, the larger corpus is not a luxury. It is a necessity.

House Down Payment (7-10 year horizon)

Property prices in Indian metros appreciate at 7-9% annually. A moderate 5-7% step-up is appropriate here because the goal amount is typically fixed (say, 20 lakh for a down payment) and the horizon is shorter. Use a step-up SIP calculator to work backward: enter the target amount, the tenure, and the expected return, then find the starting SIP and step-up percentage that reach the goal.

Quick rule of thumb: The longer the goal horizon, the more impactful the step-up. For goals under 5 years, step-up adds marginal value. For goals above 10 years, it can be the difference between hitting your target and falling 30-50% short.

Common Mistakes to Avoid with Step-Up SIP

Even a well-intentioned step-up SIP can go wrong if these five errors are not avoided:

- Choosing too high a step-up percentage. A 5,000 SIP with a 10% step-up beats a 7,000 flat SIP over 15 years. The growth rate matters more than the starting amount. But a 15-20% step-up on an 8% salary growth becomes a burden by year 5 and often leads to a complete SIP stoppage. Stick to 10% as the default unless you have strong reasons to go higher.

- Not reviewing the fund annually. A step-up SIP channels more money into the same mutual fund each year. If that fund consistently underperforms its benchmark or peer category over 2-3 consecutive years, you are increasing your investment in a poor vehicle. Review fund performance at least once a year. Switching to a better-performing fund in the same category does not reset your step-up.

- Ignoring the cap. Without a maximum monthly limit, a 10,000 SIP with 10% step-up reaches 61,159 by year 20. For investors running multiple step-up SIPs across different funds, the combined monthly outflow can snowball beyond affordability. Always set a cap at 30-40% of your current take-home income.

- Stopping the entire SIP during financial stress instead of pausing only the step-up. Most platforms let you freeze the step-up while keeping the base SIP running at its current amount. If finances are tight in a particular year, pause the increment. Do not stop the SIP itself. The cost of stopping an SIP and restarting later is enormous in lost compounding.

- Starting a step-up SIP before building an emergency fund. Sequencing matters. Build 3-6 months of expenses in a liquid fund first. Get adequate health and term insurance. Then start your step-up SIP. If you skip this order, a medical emergency or job loss in year 3 could force you to break the SIP at a market low, destroying years of compounding in a single redemption.

Frequently Asked Questions: Step-Up SIP for Indian Investors

What is the ideal step-up percentage for SIP?

For most salaried professionals in India, 10% is the recommended step-up percentage. It aligns with the average corporate salary increment range of 8-15% and comfortably outpaces CPI inflation at 5-7%. If your income growth is slower or less predictable (freelancers, business owners), start with 5%. The most important consideration is sustainability. A percentage you can maintain for 10-15 years without stopping the SIP will always outperform an aggressive percentage that leads to abandonment in year 3-4.

Can I change or stop the step-up after starting?

Yes. All major platforms including Groww, Zerodha Coin, Kuvera, and Paytm Money allow you to modify, pause, or completely remove the step-up instruction at any time. Crucially, pausing the step-up does not stop your base SIP. Your monthly investment continues at its current amount. You can restart the step-up later when your financial situation improves. This flexibility is one of the strongest advantages of the step-up SIP structure.

Is step-up SIP better than increasing SIP manually every year?

Both approaches produce the same result mathematically. The advantage of automatic step-up is entirely behavioral: it removes the annual decision point. Many investors plan to increase manually each April but forget, postpone, or talk themselves out of it when the month arrives. Automation ensures the increase happens without requiring willpower or a calendar reminder. That said, if your platform does not support auto step-up, manual increases work perfectly well. Just treat the annual increase as non-negotiable and execute it within the first week of your increment month.

How much corpus can a 10,000 step-up SIP create in 20 years?

At 12% assumed annual return with a 10% yearly step-up, a 10,000/month starting SIP grows to approximately 1.99 crore in 20 years. The total invested amount across the 20-year period is approximately 68.73 lakh. Without step-up, the same starting SIP creates approximately 1 crore on a total investment of 24 lakh. The step-up nearly doubles the final corpus. For a 25-year horizon with the same parameters, the step-up corpus reaches approximately 4.7 crore compared to 1.88 crore for the flat SIP.

Does step-up SIP work for debt mutual funds?

Technically, you can set up a step-up SIP in any mutual fund scheme, including debt funds. But the practical benefit is limited. Debt fund returns are lower (6-8% annually for most categories) and NAV volatility is minimal, so the compounding effect of increased contributions does not create the same dramatic difference as in equity funds. Step-up SIP shows its real power in equity and hybrid fund categories where long-term returns are higher (10-14%) and compounding periods are longer. For debt funds, a flat SIP or lump sum is usually sufficient.

Start Small, Step Up, Stay Invested

Step-up SIP is the simplest and most effective adjustment an Indian investor can make to an existing SIP strategy. It requires no market timing, no fund-switching, and no extra effort beyond a one-time setup. A 10% annual step-up on a 10,000/month SIP nearly doubles the 20-year corpus from approximately 1 crore to 1.99 crore.

The math confirms what common sense suggests: if your income grows every year, your investments should too. A flat SIP ignores this reality and leaves significant wealth on the table over a 15-20 year horizon.

If you already have a running SIP, log into your platform today and add the step-up instruction. If you are starting fresh, configure the step-up from day one. Sync it with your appraisal month. Set a cap at 30-40% of current income. Choose a diversified equity fund. And most importantly, choose a step-up percentage you will not abandon during a tough year.

AMFI data shows SIP monthly inflows near record levels at 30,953 crore (May 2026), but the stoppage ratio above 100% in March and April 2026 is a warning: sustainability matters more than ambition. The best step-up SIP is the one that runs for 15 years, not the one with the highest percentage that stops after 3.